Is a HELOC a Good Idea?

Key Takeaways

-

- A Home Equity Line of Credit (HELOC) is a flexible way to borrow money secured by the equity you have in your home.

- Getting approved for a HELOC depends on your home’s value, what you owe on your mortgage, and other factors such as your credit score, income, and debt-to-income ratio.

- A HELOC has risks since your home is used as collateral, so understanding the draw period, repayment period, and interest rates is critical.

- A Home Equity Line of Credit (HELOC) is a flexible way to borrow money secured by the equity you have in your home.

If you’re a homeowner, you might be asking: “Is a HELOC a good idea?” A Home Equity Line of Credit (HELOC) can be a smart financial tool, but it’s important to understand exactly how borrowing against your home’s equity works before you apply.

A HELOC is a revolving line of credit secured by the equity in your house. HELOCs often have lower interest rates than personal loans or credit cards, potentially making a HELOC a smart way to borrow.

You’re approved for a set amount, but you only pay interest on what you actually use. During the draw period, you can borrow as needed and make minimum monthly payments. When the draw period ends—usually after 5 to 15 years—the repayment period begins, and you must repay the remaining balance plus interest. For homeowners who want predictable monthly payments, Lake City Bank also offers a Fixed Rate Lock on your HELOC, which combines the flexibility of a line of credit with a stable, fixed interest rate.

Key HELOC benefits and risks

With a HELOC, you use your home’s equity to help you borrow money at a favorable rate to finance other goals you may have.

Some common uses for HELOCs include:

- Paying off higher-interest debt like credit cards

- Financing home improvements or home renovations, including kitchen or bathroom upgrades

- Buying big-ticket items such as a car

- Covering college expenses

Risks to consider:

- Your home is used as collateral—defaulting on a HELOC could put your home at risk.

- Interest rates on HELOCs can be variable, meaning payments may rise over time.

- Borrowing more than you can reasonably repay may increase the likelihood of financial hardship or missed payments.

How to qualify for a HELOC

Getting approved for a HELOC depends on your home’s value, how much you owe on your mortgage, how much you want to borrow, and your credit profile, including your credit score and debt-to-income ratio. To determine if you qualify and how much you can borrow, follow these steps:

Determine your equity

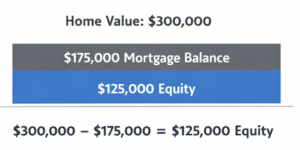

HELOCs are based on the equity in your home. To determine your home equity, subtract your mortgage balance from your home’s market (or appraised) value (Note: you may have to obtain a new appraisal for this step).

Example:

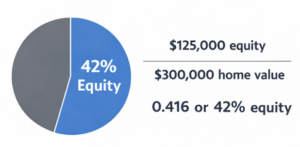

Divide equity by your home’s value to determine equity as a percentage. Most lenders require equity of 15% to 20% for a HELOC.

Calculate Combined Loan-to-Value

Another calculation lenders review is your Combined Loan-to-Value, or CLTV. Combine what you want to borrow with your mortgage balance. Divide the total by your home value. Most lenders require a maximum of 75% to 85% CLTV to qualify for a HELOC.

So, is a HELOC a good idea?

Before borrowing, always review your budget to determine if the additional payments will fit comfortably in your plans, especially since HELOCs use your home as collateral. If you’re disciplined with borrowing and clear on your repayment plan, a HELOC can be a smart, flexible line of credit to support your financial goals.

All loans are subject to credit approval.